"Invert, always invert": why would the economy continue to grow?

Why isn't the economy in a steady state yet?

“Invert, always invert: turn a situation or problem upside down upside down. Look at it backward.” - Charlie Munger

In Growth, by Process of Elimination ($), Byrne Hobart describes that a clever way to understand growth companies is to ask why they didn’t reach their steady state yet.

One way to think about growth companies, or growth stocks, is to work backwards from this model: if there's a good explanation for why a company hasn't reached its steady state yet, and that explanation is not managerial incompetence, then by process of elimination the only outcome you can expect is further growth. If volatile stagnation is the default case, then making a credible argument for steady above-average growth means listing things almost all companies have in common and then spotting instances where the company in question doesn't fit the model.

Although Hobart only mentions companies, it’s worthwhile to ask: why didn’t the economy achieve its steady state?

This is also one of my first attempts to address one of my working theories: the last 2 centuries are aberrations and total outliers both in terms of economic growth and progress and what we’re going through is a step change, not a growth change in the economic growth of our societies.

In the past, stagnation was the norm

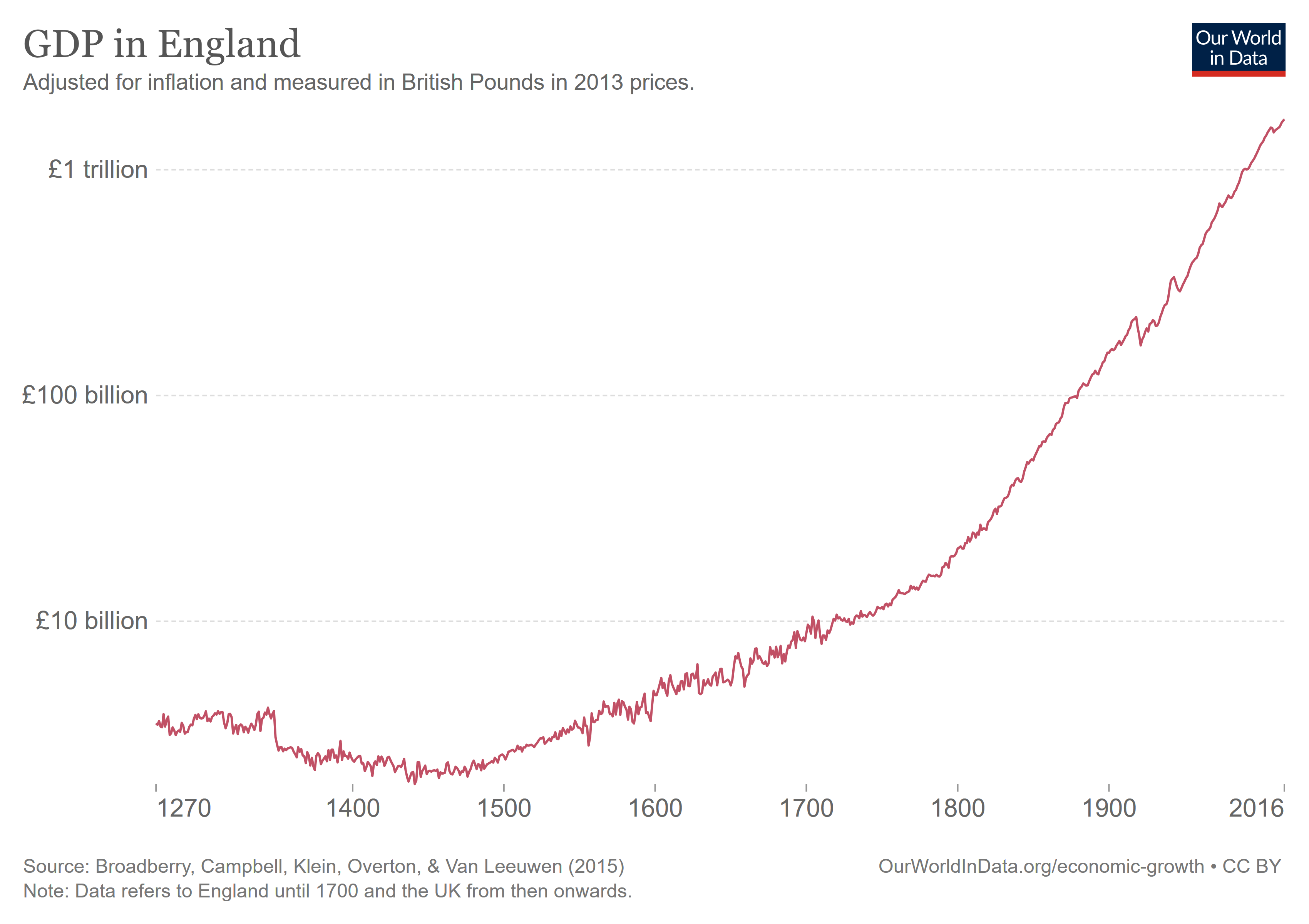

According to data compiled by Our World in Data, between 1345 and 1575 England's GDP was flat. This is a shocking surprise if you think that between these 240 years, the printing press was invented, America was discovered and a significant number of low-hanging fruits there were discovered.

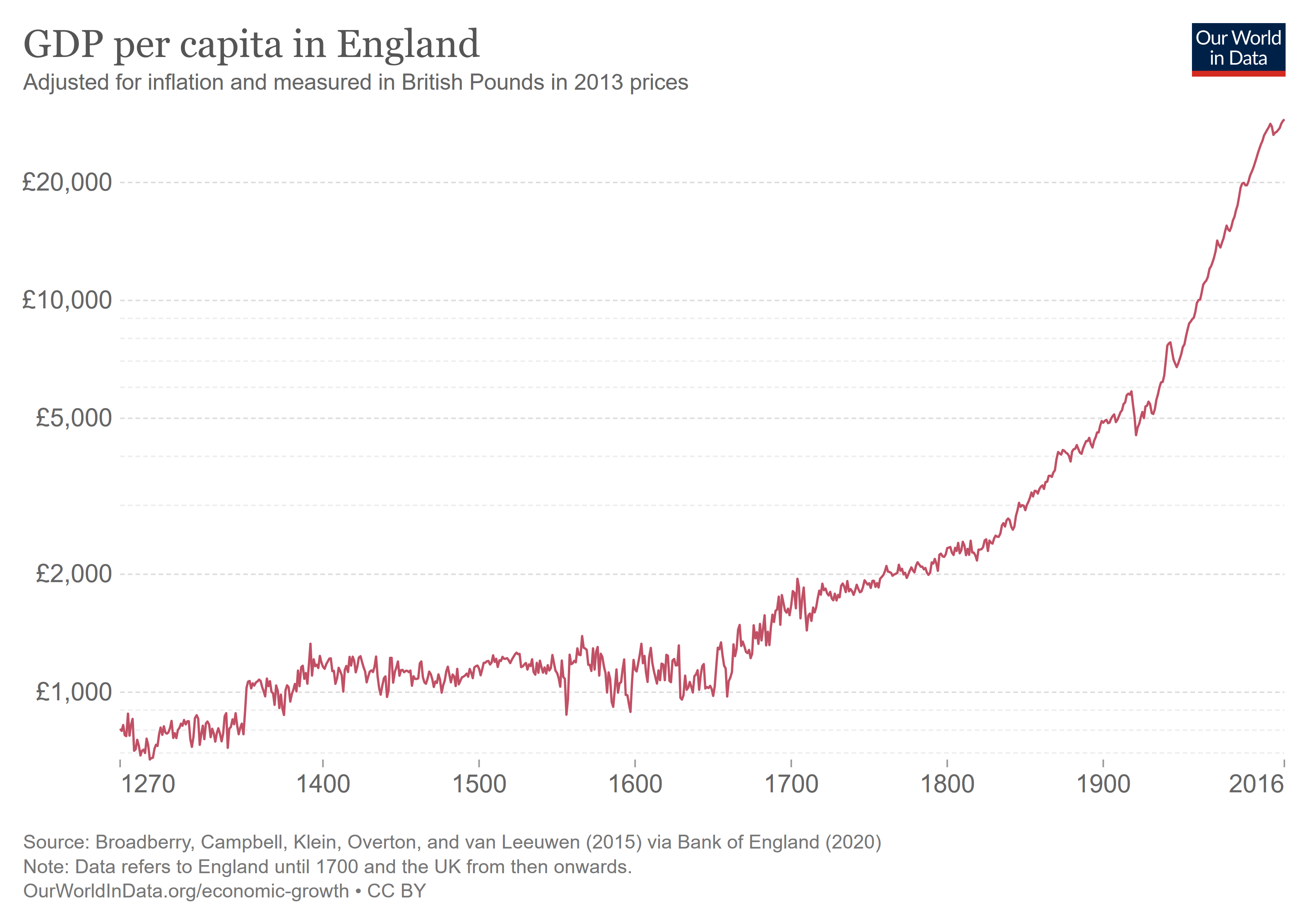

Between 1500 and 1800 the England/UK economy grew 0.7% per year.

Of course, the main reason past economies were smaller is that there were fewer people in the economy back then. Particularly, there were fewer working-age populations, either because of wars, lack of public health goods, or simply because of high levels of child mortality.

Therefore, although the England/UK economy would grow 0.7% per year over these periods, the per capita GDP only grew 0.2% per year, meaning that much of the growth came from more people living in the UK.

It makes sense, making more with the same inputs is hard stuff to do.

More recently, a new trend has begun that all people just assume that growth will continue perpetually. It can be a recency bias (I am unaware of another central bank that reports GDP data for a millennium. Most countries don’t do that because they don’t exist for millennia, or they had big revolutions in the meanwhile that disrupted everything. Therefore, if you’re studying the American economy, it’s hard not to extrapolate data since 1789 and think “I think that it’s just a thing Americans do, they grow their economy forever”.

A slightly less foolish take would be something like “of course we won’t grow GDP forever, but it’s a trend that is going on for such a long time that it’s a good bet to say it’ll continue to happen over the next 45 years until I spend all my savings in my retirement account”

Indefinite optimism

From Blake Masters and Peter Thiel 2014 book Zero to One:

After a brief pessimistic phase in the 1970s, indefinite optimism has dominated American thinking ever since 1982, when a long bull market began and finance eclipsed engineering as the way to approach the future. To an indefinite optimist, the future will be better, but he doesn’t know how exactly, so he won’t make any specific plans. He expects to profit from the future but sees no reason to design it concretely.

Instead of working for years to build a new product, indefinite optimists rearrange already-invented ones. (…)

Recent graduates’ parents often cheer them on the established path. The strange history of the Baby Boom produced a generation of indefinite optimists so used to effortless progress that they feel entitled to it. Whether you were born in 1945 or 1950 or 1955, things got better every year for the first 18 years of your life, and it had nothing to do with you. Technological advance seemed to accelerate automatically, so the Boomers grew up with great expectations but few specific plans for how to fulfill them. Then, when technological progress stalled in the 1970s, increasing income inequality came to the rescue of the most elite Boomers.

The core idea of Thiel's thinking is that we stopped building new things and the recent growth in the economy was boosted by some mix of population growth, information technology (that isn’t real technology for him, for some reason), and falling rates. Even if the internet was a thing in 1982, you couldn’t make PayPal give money away to lure customers to your product like Thiel did because money used to cost too much back then.

Is tech stalled?

I never understood why Thiel thinks information technology doesn’t count, but this debate is getting old because: Jack Kirby invented the integrated circuit in 1958, Intel launched the microprocessor in 1971 and Apple launched the iPhone in 2007, 15 years ago. Carlota Perez, in her excellent book Technological Revolutions and Financials Markets lays out a 50-70 year cycle for a technological revolution and 2021 was exactly the year that the current revolution had its 50th anniversary.

From her 2007 paper Great Surges of development and alternative forms of globalization:

However, in the latter phase of this period, many of the products and industries of the revolution are approaching maturity, restricting the growth of productivity, markets and profits. This creates the conditions for social and political unrest in the core countries, migration of markets and production activities to the peripheries, and the search for new technologies that leads to the next big-bang and a new great surge of development.

And the stuff that Perez predicted in 2003 are happening:

{kind=link}

In my humble opinion, There are other writing on the walls that we’re approaching the end of this revolution.

It’s possible that you’re familiar with the Carlota Perez work because of some crypto bro trying to pitch you that crypto is the next big thing (the search Carlota Perez Bitcoin has 146,000 results on Google). It isn’t.

What could the economy continue to grow?

Even though the 5 technological revolutions that Perez describes on her book are a big part of the recent growth over the last ~200 years, those aren’t the whole story. We created inclusive institutions, many improvements in health sciences allowed people to live for longer1, women joined the workforce doubling it, we got one off gains teaching people to read, and we created financial markets that help people to save and deploy capital more efficiently. All of that is kind of outside of the pure technological progress GDP growth were discussing here, but during the 21st century it seems likely that those dynamics are likely to be turn into headwinds. In most developed economies, the workforce decreases as people age without having 2 kids to replace them.

But if you are like me and you work at a TMT fund (or more broadly, you choose a career in tech), you’re making an indefinite optimistic bet: the information technology revolution must go on. If more broadly, you live in our society, everything on financial markets, from valuations to how people calculate the solvency of countries is downstream from perpetual GDP growth.

There are three distinct possibilities:

The current revolution still has legs to go

We’re going to have a second run of sort of the same thing, but different and more complex.2 Maybe AI or Virtual Reality?

A different thing. Like the first four had some element of energy and Transporation, maybe the next one will be rocket science?

I need to confess I am a bit skeptical of these three. Cathie Wood is a famous investor that sells innovation as an investment thesis and every year she makes this presentation where she lists all the big ideas for the future. Because she spends so much time thinking about this stuff, the list she makes should be a nearly exhaustive list of all the stuff that could be 2 or 3:

I am skeptical on all of these as the next really big thing, maybe a little more neutral on AI… I also don’t think that health care has what is needed to be the steward of GDP growth.3

I want to leave open the possibility that the move to a carbon free society can have something there, particularly if you have what is needed to export green hydrogen but not much of oil. But globally, it should be only a matter of replacing one thing by other: zero sum.4

Invert, always invert

If Hobert says you should invert why a company didn’t reach saturation (e.g.: AWS will still grow because moving workloads to the cloud takes time and only 25% were moved yet), why didn’t we achieve the steady state of a rich very slow changing society where the future looks like the past? What this society would look like and what is left?

Abundant and cheap energy

Robots to make stuff for us

Faster transportation (perhaps powered by the cheap energy?)

More connectedness and more information5

Healthy long lives

One important tidbit is that you should think about every inversion not in terms of what science fiction authors describe these utopias, but what would be the saturation level, in both terms of the laws of physics but also of human psychology6. It's also possible that certain stuff that enables other don't make economic sense. If we 100x our energy output right now, will we find useful things or will use the remaining capacity to mine Bitcoin? Will people want to live happy lives if suddenly dying at age 150 is the new normal?

I need to admit that I’m not exactly sure about what is missing in the world that could make a 6th technological revolution over the next 50-60 years.

Yes, some stuff would be revolutionary, like a pill of long life. But it seems decades if not centuries away. Fusion is always 20 years away. For robots, the robot revolution has already happened. My rule of thumb is that at this point, anything possible of being automated by a robot, Amazon already did it.

The same would apply for Toyota

Alternatively, the Whalton family don’t run a charity and if they employ 2.3M people, it’s because restocking shelves must be a really hard job for robots to make economically.

Of course, we still have a good runway in front of us, even if we don’t have much technological progress. 3.3B people live under $5.50 a day. One could imagine all of them eating at the McDonald’s, using air conditioners, drinking Coke, buying iPhones, and driving Corollas eventually. Lots of them, mostly in south and southeast asia are getting rich and will drive more consumption.

I am not calling for the economy to go ex-growth tomorrow. The U.S. economy grew 23% over the last 10 years. It is reasonable to imagine the trend to continue for a decade, even if at a lower rhythm. At a 23% growth per decade, the economy doubles in size every 34 years. At the same time, because I plan to live 68 years more, I will be surprised if the U.S. economy is 4x larger by 2090.

But when I think about a theoretical steady state economy and where we are, these two realities are remarkably close. What else does our modern society need?

Even though the Germ theory of disease was only invented in the late 19th century and there must be reasons that link it to the 3rd technological revolution somehow, it is something that could be discovered in some ancient metropolis like Rome.

The second technological revolution, the Age of Steam, was in good part about Steam Engine Railroads while the third was about Steal was about Heavy Engineering, where they built even more railroads.

This is all opinion if you didn’t notice. My skepticism with health care is simply because despite of the massive run we had during the last five revolutions; health care wasn’t the protagonist on any. Bank of Communications, China’s 4th largest bank, has this name because the word communications in Chinese also means transportation, and BoCom was founded in the early 20th century to fund railway construction. All the 5 revolutions either were about making better transportation or about information, with some energy angle. I think we would need immortality stuff here to change the economy materially in the levels I am talking about here.

One could say that through technology, we could become very good in making cheap energy with renewables. But the truth is that hydrocarbons are the cheapest form of energy and it is incredibly cheap already. In a regular year, you can spend as low as 5% of GDP in energy cost. How much economic activity aren’t done because energy is too expensive but would be expensive if it were 2% of GDP? My gut says: not much.

Basically, Meta’s bull case

For certain stuff, it’s possible that we have the technology for it, but we won’t see adoption. You can spend your life in VR already.