I might have changed my mind: passive might be destroying price discovery

I tried to write a post dunking on the people who complain about price discovery and failed.

For those that follow me on X, you might be aware that I have been keenly oppositional of people who complain about passive investing.

Or more recently with regards to Akre letter:

I even wrote a Substack draft in April titled “Are equity markets broken? - A response to Akre”, but I decided to not publish it, because I have found a good argument, and I want to share it here with you.

One caveat. I have never seen this argument before. I am certain I’m not the first person to have thought about it, but when you see big opposition to passive investing, they never make a good argument explaining the mechanism.

So here it is.

Thesis creep

Let’s say you own two stocks: The Coca-Cola Company and NVIDIA Corp. You own them because you think they are undervalued, why else would you own them?

One day, you wake up and you see that NVDA is up +4% for no good reason. Well, it’s a big secular thesis, maybe some boutique just published their work in the Taiwan supply chain. Or retail is pushing. But you don’t get too uncomfortable. If you’re paying 36x NTM Earnings, a 2.8% yield, seriously: Will you now cut your stock just because it’s trading at 37.4x NTM Earnings, or a 2.7% yield?

No, you won’t.

People have been wrong before underestimating Nvidia. You have been wrong before underestimating Nvidia. It’s a fast-moving name, perhaps Nvidia did some presentation in an industry conference you weren’t aware of. Or a competitor. I mean, if Lisa Su said she can’t make enough MI300s, you’d be optimist, right? Who knows? You don’t even speak Mandarim to follow the Taiwanese media. Just let your winners run.

And so it runs. +4% today, +1% tomorrow, +3% next week, these numbers compound. And suddenly the stock is up 40%, it’s overvalued according to your initial estimation, and you didn’t sell one single share. You know there’s a big dispersion, but it’s skewed to the upside. And even if the stock is overvalued, you trim a bit, but mostly stays long.

Then you read some new thesis. Things are even better than previously thought. You update your exit multiple. Then you keep the same growth rates from a higher base. And suddenly, you are justifying the new price.

But what if people bid Coca-Cola out of nowhere? It’s up 4% in the day, suddenly, it’s up 40% in six months. What do you do?

Coca-Cola is a very mature business. Margins are super optimized. Everyone that could want to drink a Coke, already drinks. And you’re smart, but you know you’re not THAT smart. What are the odds you bought KO at 70 cents on the dollar? Zero, right? If it’s up 40%, it has to be overvalued, you think.

If someone comes up and says “hey, I think this new sweetener is a game changer”, you’ll say “no way, they have gone through many sweeteners. If something changes, it’s going to be through the great arc of time. Consumer behavior is very rigid. Don’t be silly. It’s Coke, not Nvidia.”

You sell. Obviously.

Non-speculative stocks have inelastic supply

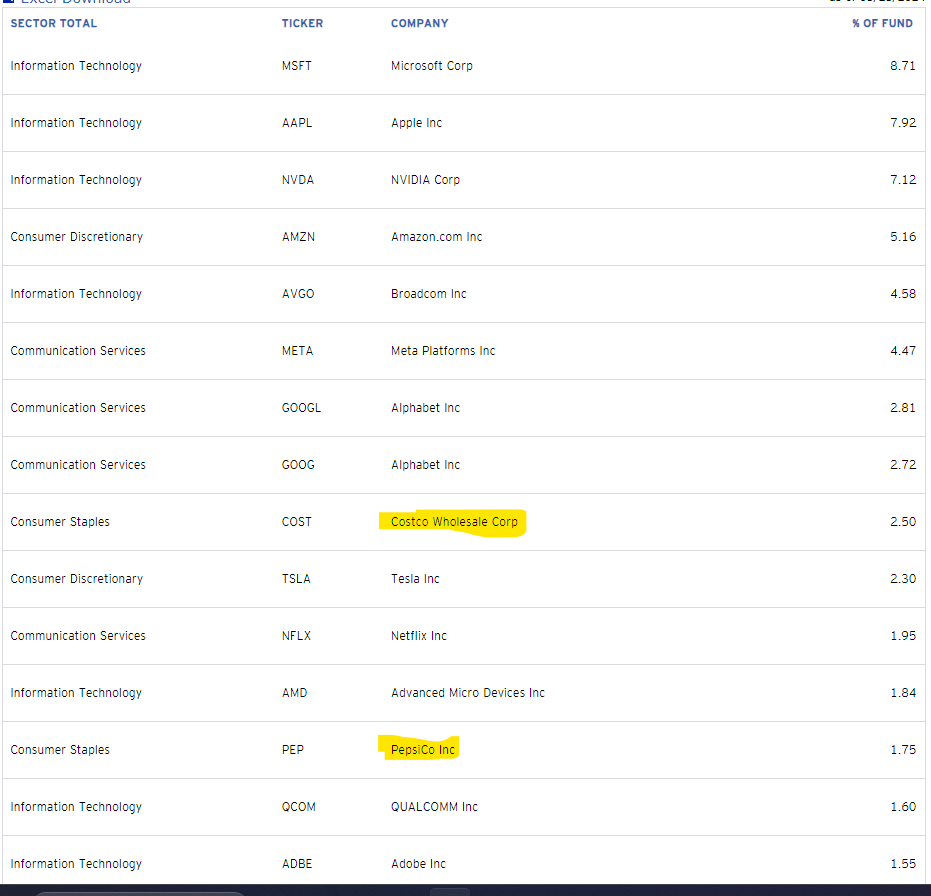

For many historical reasons, people like to own the stocks that are primarily listed on the Nasdaq exchange, and not the ones primarily listed on the New York Exchange. This is primarily because technology companies like to list in the Nasdaq. But instead of buying some technology index, like the S&P North America Expanded Tech Sector ETF (IGM), people like to invest and benchmark themselves against the Nasdaq-100 Index, a capitalization-weighted (but adjusted) index of the one hundred largest companies in the Nasdaq. The clever people at Invesco created the QQQ, a passively ETF that tracks the Nasdaq-100. Only Invesco holds more than $300B in AuM tracking the Nasdaq-100.

But companies like PepsiCo and CostCo aren’t technology stocks!

Let’s see their performance in the past year, a good year for tech stocks.

Nasdaq-100: +35%

PepsiCo: -3%

CostCo: +66%

Let’s think how PepsiCo shareholders think when the tech stock bid comes through the QQQ:

“Muhahahah. These dumb tech investors are buying the QQQ again, the QQQ is buying all stocks in accordance with the index, and the guy is getting more PEP than Qualcomm. And they are driving PEP price up, again. Better sell my stocks for them before this technology bubble pops.”

Costco is different. It is more like a cult stock. The Omaha mafia love it! The late Charlie Munger always spent long hours saying good things about Costco. And even before this last run up, the company delivered. Up 1950% in the 20 years ended in May 24th 2023, versus 350% for the S&P 500.

CostCo price to earnings went from 32x NTM to 49x. +53%!

It’s possible that Costco investors have learned all the same lessons that Nvidia investors learned above1: Costco always surprises to the upside, let your winners run, the business is on another level and deserves a super multiple, and so on.

The point is: when Costco stock goes up, Costco investors don’t get super anxious about it and rush to sell, they are used to Costco stock going up.

The step by step

The passive bid happens.

The bid is met with resistance by current shareholders of companies that are perceived to be of low uncertainty and upside risk.

You don’t need to move the price of the non-speculative stocks by much to buy the desired shares for the passive bid.

The bid isn’t met with resistance by shareholders of companies are perceived to be harder to forecast and with more upside risk. Including companies with good momentum.

You need to move the price of these companies by a lot to buy the desired shares you need.

Passive messes with price discovery, making the market overweight the most speculative names

Conclusion

I’m not certain I totally believe in this. I might?!

I also don’t know exactly what to do with this information, even if it is true. Should I be long speculative momentum ad infinitum? Probably not.

The argument makes sense, but it’s hard to imagine the degree to which it happens. You can believe in my first principles reasoning. Or you can believe in Michael J. Mauboussin: go read Looking for Easy Games - How Passive Investing Shapes Active Management. Who’s more likely to be right? Me or Michael Mauboussin?

Luckly, someone can point to some paper, or do a paper, or a study, trying to use some heuristic for the speculative level of the stock (analyst forecast dispersion, volatility, momentum, beta, etc), for the direction and dimension of the passive bid, and trying to control for companies that are in and out of the main passive indexes. For example, TSM is out of the QQQ, but NVDA is in. CRM, ORCL, and SAP are out of the QQQ, but ADBE, MSFT, INTU, and ADP are in. And obviously there’s the S&P 500.

I plan to update my view on this throughout the years based on hard evidence.

But I’m not doing this study or looking for one this time.

Next time you want to do like Einhorn and blame Blackrock for your own underperformance, make this argument. Everyone will love you talking about elasticity. And you’ll look clever.

From page 10 of the 2021 Sempter Augustus letter: “But as with Ross, every decision to sell a Costco share would have been a mistake—until now, in our estimation. We never would have expected the shares to trade at today’s price. However, as some shares do still reside in some client accounts, we will deliberately scale back in at more reasonable price points. Borrowing from a former seven-time Mr. Olympia, ‘We’ll be back.’”